When it comes to buying a property in the UAE, understanding the difference between a mortgage and a home loan is essential. Both terms are often used interchangeably, but in reality, they serve different purposes, have unique structures, and cater to specific financial needs. In this comprehensive guide, we explore the key differences between a mortgage and a home loan in the UAE, their eligibility requirements, benefits, and which one might be the better choice for your real estate goals.

What Is a Mortgage in the UAE?

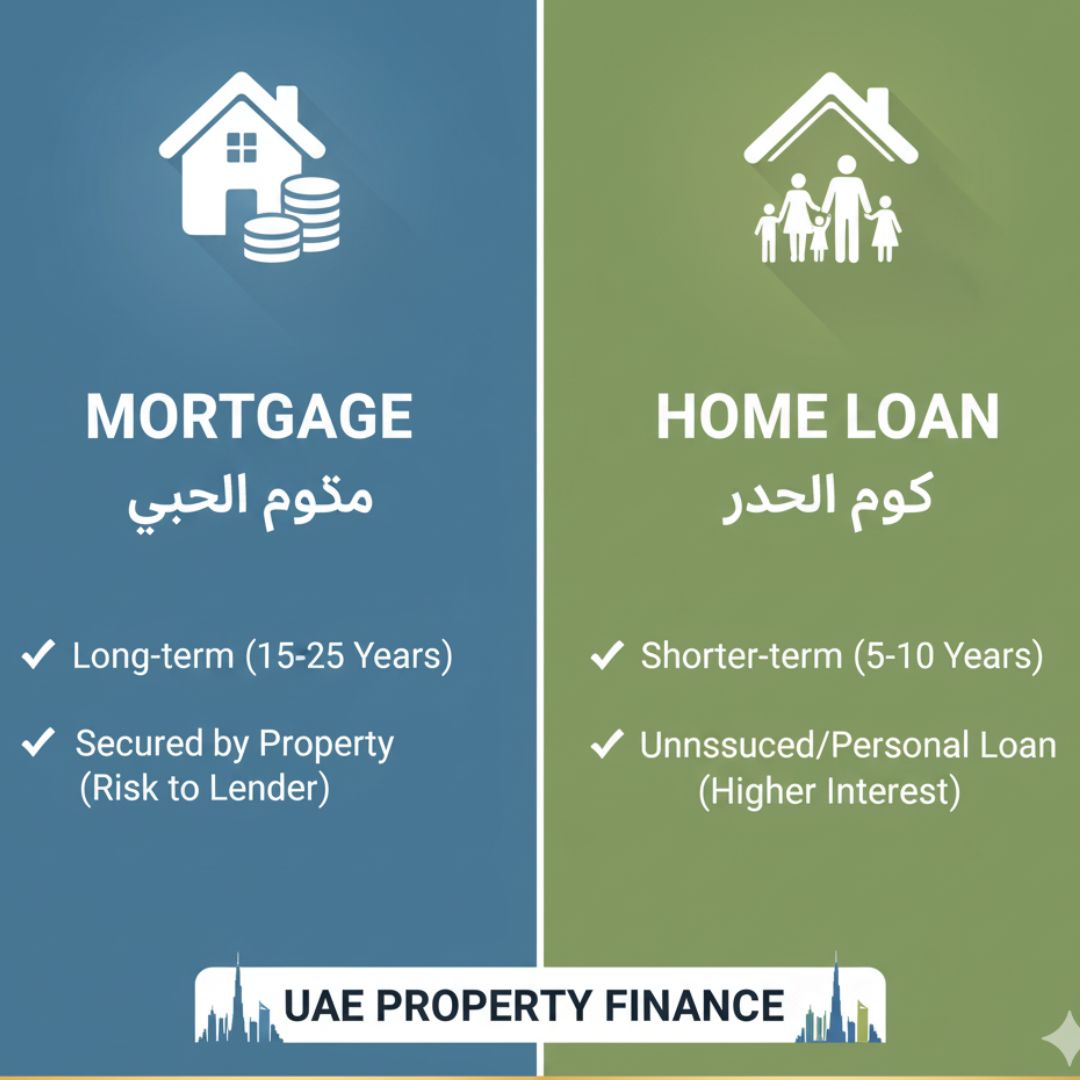

A mortgage is a secured loan that enables individuals to purchase a property while using that same property as collateral. In the UAE, banks and financial institutions provide mortgages to both UAE nationals and expatriates, allowing them to finance up to 80–85% of the property’s value.

The property ownership remains with the buyer, but the bank holds a lien on it until the mortgage is fully repaid. This means that if the borrower fails to make payments, the lender can seize the property to recover the loan amount.

Key characteristics of a mortgage in the UAE include:

-

Long repayment tenure (up to 25 years)

-

Fixed or variable interest rates

-

Legal documentation and property evaluation required

-

Applicable for ready and off-plan properties

Mortgages are ideal for individuals looking to purchase residential or commercial properties for investment or personal use.

What Is a Home Loan in the UAE?

A home loan, while similar in concept, is a broader term that includes different types of financing for housing-related expenses. In many cases, a home loan can cover construction, renovation, or home improvement, not just the purchase of property.

In the UAE, home loans are typically offered under mortgage frameworks, but some banks differentiate between purchase mortgages and home improvement loans. The latter are usually unsecured or partially secured, depending on the borrower’s profile and credit score.

Key features of home loans in the UAE include:

-

Covers construction, renovation, or extension costs

-

May not always require full property collateral

-

Shorter repayment tenure than standard mortgages

-

Higher interest rates for unsecured loans

Mortgage vs Home Loan: The Core Difference

The main difference between a mortgage and a home loan in the UAE lies in purpose and collateral. A mortgage is always secured by the property being purchased, while a home loan may or may not involve property as security.

| Factor | Mortgage | Home Loan |

|---|---|---|

| Purpose | To purchase a property | To build, renovate, or improve a property |

| Collateral | Property purchased | May or may not be secured |

| Tenure | Up to 25 years | Usually 5–15 years |

| Interest Rate | Lower (secured loan) | Higher (unsecured loan) |

| Loan Amount | Based on property value | Based on borrower’s income and creditworthiness |

| Ownership | Bank holds lien until repayment | Full ownership may remain with borrower |

In short, while a mortgage focuses on property acquisition, a home loan caters to property enhancement or development.

Types of Mortgages Available in the UAE

There are several types of mortgages tailored to different financial needs and goals.

1. Fixed-Rate Mortgage

The interest rate remains constant throughout the loan period, offering predictable monthly payments. Ideal for those who prefer financial stability.

2. Variable-Rate Mortgage

The interest rate fluctuates based on the UAE Central Bank’s EIBOR rates. It’s suitable for borrowers who can tolerate market volatility in exchange for possible savings during low-interest periods.

3. Offset Mortgage

This type links the borrower’s savings or current account to the mortgage. Any balance in the linked account helps reduce interest payments on the outstanding loan.

4. Islamic Mortgage (Sharia-Compliant)

Under Islamic banking principles, interest (riba) is prohibited. Instead, banks offer Ijara (lease-based) or Murabaha (cost-plus financing) structures, where the bank buys the property and leases or resells it to the borrower at an agreed profit margin.

Eligibility Criteria for Mortgages and Home Loans in the UAE

Whether applying for a mortgage or a home loan, borrowers must meet specific eligibility requirements set by UAE banks.

Basic criteria include:

-

Minimum monthly income: AED 10,000 to AED 15,000

-

Stable employment or verified business income

-

Valid UAE residency visa (for expatriates)

-

Minimum age: 21 years

-

Credit score above 650 (AECB)

Most banks require a down payment of 15–25% for expatriates and 10–20% for UAE nationals. The loan-to-value (LTV) ratio varies depending on the property type and buyer’s profile.

Documents Required

Applicants must provide the following:

-

Copy of Emirates ID and passport

-

Salary certificate or trade license

-

Recent bank statements (3–6 months)

-

Property sale agreement or title deed

-

Proof of down payment

Additional documentation may be required for self-employed applicants or off-plan properties.

Interest Rates and Repayment Terms

In the UAE, mortgage interest rates typically range between 3.5% to 5.5% per annum, depending on the bank and borrower’s profile. Home loans, especially unsecured ones, can have higher rates of 5% to 7%.

Repayment terms for mortgages can extend up to 25 years, whereas home loans generally range from 5 to 15 years. Borrowers may choose between fixed, variable, or hybrid interest structures to manage risk and flexibility.

Pros and Cons of Mortgages and Home Loans

Mortgage Pros

-

Lower interest rates

-

Long repayment tenure

-

Ideal for property investment

-

Can leverage property appreciation

Mortgage Cons

-

Requires collateral

-

Longer approval process

-

Penalties for early settlement

Home Loan Pros

-

Flexible usage (renovation, construction)

-

Quicker approval for smaller amounts

-

Suitable for homeowners improving existing properties

Home Loan Cons

-

Higher interest rates

-

Shorter repayment periods

-

May require strong credit profile

Which Is Better: Mortgage or Home Loan in the UAE?

Choosing between a mortgage and a home loan depends on your financial objective.

If your goal is to buy a new property, a mortgage is the right choice—it provides access to higher funding with manageable interest rates and extended tenures.

However, if you already own a property and wish to upgrade, renovate, or expand, a home loan might be more suitable due to its flexible purpose and faster processing.

For expatriates investing in UAE real estate, mortgages offer an excellent opportunity to own property without full upfront payment, making them a cornerstone of property financing in the Emirates.

FAQs

1. What is the main difference between a mortgage and a home loan in the UAE?

A mortgage is used to purchase property and is secured by that property, while a home loan can also cover construction or renovation and may not always require collateral.

2. Can expatriates get a mortgage in the UAE?

Yes, most UAE banks offer mortgages to expatriates with a valid residency visa, steady income, and a minimum down payment of 15–25%.

3. Which is better: a mortgage or a home loan in the UAE?

If you’re buying a property, a mortgage is better. If you want funds for renovation or construction, a home loan is more suitable.

4. What are the typical mortgage interest rates in the UAE?

Mortgage interest rates in the UAE usually range from 3.5% to 5.5%, depending on the bank and borrower profile.

5. How long is the repayment period for a mortgage in the UAE?

Mortgage repayment terms can extend up to 25 years, while home loans typically have shorter terms of 5–15 years.

Conclusion

Understanding the difference between a mortgage and a home loan in the UAE is crucial for making informed financial decisions. Mortgages are best suited for purchasing properties, while home loans are ideal for construction and renovation projects. Both play a pivotal role in helping residents and expatriates achieve their homeownership goals in one of the most dynamic real estate markets in the world.

If you’re considering applying for either, always compare interest rates, tenure, and bank policies to ensure the best fit for your budget and long-term plans.

Leave A Comment

You must be <a href="https://7seasmortgage.com/wp-login.php?redirect_to=https%3A%2F%2F7seasmortgage.com%2Fmortgage-vs-home-loan-difference-in-uae%2F">logged in</a> to post a comment.